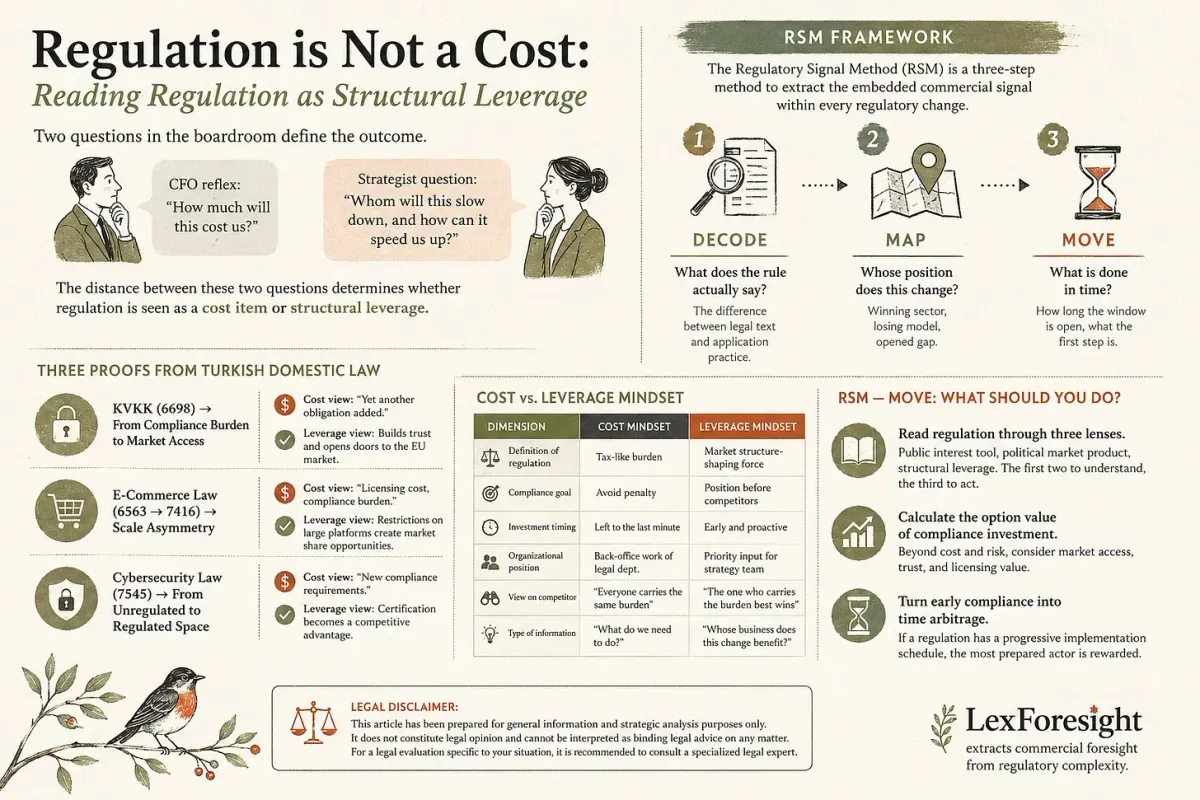

Regulation is Not a Cost: Reading Regulation as Structural Leverage

When “new regulation” is mentioned in a board meeting, two types of reactions occur in the room. First, the CFO reflex: “How much will this cost us?” Second — the strategist question: “Whom will this slow down, and how can it speed us up?”

The distance between these two questions determines whether a company views regulation as a cost item or structural leverage. And this difference in perspective explains why two competing companies operating in the same regulatory environment achieve dramatically different results.

Thanks for reading LexForesight! Subscribe for free to receive new posts and support my work.

What is the Regulatory Signal Method (RSM)?

This article — and all analyses in this series — is structured around the Regulatory Signal Method (RSM) framework. RSM is a three-step reading method to extract the embedded commercial signal within every regulatory change:

- DECODE: What does the rule actually say? (The difference between legal text and application practice)

- MAP: Whose position does this change? (Winning sector, losing model, opened gap)

- MOVE: What is done in time? (How long the window is open, what the first step is)

In this article, we will read KVKK, e-commerce, and cybersecurity regulations through these three steps.

RSM — DECODE: Three Faces of Regulation

1. Classical Definition: Public Interest

The most common definition of regulation is based on public interest theory. The state intervenes to correct market failures. The OECD formalizes this as follows:

“Regulatory policy is the process by which government defines policy objectives, decides whether to use regulation as a tool to achieve these, and then designs and adopts regulations through evidence-based decision-making.”

— OECD, Recommendation of the Council on Regulatory Policy and Governance (2012)

Most law school curricula and compliance departments work with this perspective. Regulation is a neutral tool: there is a problem, the state solves it.

2. Critical Definition: Regulatory Capture

George Stigler, in his 1971 paper “The Theory of Economic Regulation”, dropped a bomb on this optimistic picture. According to Stigler, regulation is a product demanded by the industry itself and designed for its benefit. The basic resource of the state is the “power to coerce,” and various interest groups compete to control this power.

From this perspective, regulation:

- Restricts market entry to protect incumbent players

- Limits competition by setting price floors/ceilings

- Consolidates existing business models by blocking substitute products

Critical takeaway: If regulation is already a good produced in a political market, then it is possible to be a conscious consumer of this good instead of just a passive buyer.

3. Strategic Definition: Structural Leverage

According to the Porter Hypothesis put forward by Michael Porter and Claas van der Linde in 1995, well-designed regulations trigger innovation, and this innovation can yield productivity gains that offset compliance costs.

Two versions of the Porter Hypothesis:

- Weak: Strict regulation triggers innovation (more R&D, patents). Strong empirical support exists.

- Strong: Innovation gains exceed compliance costs. Debated, context-dependent.

The thesis of this article extends Porter: In every regulatory area — data protection, finance, e-commerce, AI — strict regulations create an asymmetric advantage for the actor that complies first and best.

RSM — MAP: The Brussels Effect and Position Shift

Anu Bradford, a professor at Columbia Law School, conceptualized the “Brussels Effect”, which demonstrates how structural leverage works on a global scale:

- Market size: The EU is one of the world’s largest consumer markets

- Economies of scale pressure: Multinational companies adopt EU standards as a global baseline instead of setting up separate production lines

- Legal emulation: Governments outside the EU voluntarily import EU standards

GDPR is the clearest example. The same dynamic is at play for the AI Act, Digital Markets Act (DMA), and Corporate Sustainability Reporting Directive (CSRD).

Strategic result: When a Turkish company complies early with EU regulation, it not only gains access to the EU market; it also opens a time arbitrage window against competitors that have not yet complied.

Three Proofs from Turkish Domestic Law

KVKK (6698) → From Compliance Burden to Market Access

The Law on the Protection of Personal Data No. 6698 was initially seen as a pure cost: data inventory, explicit consent mechanisms, VERBIS registration. However, the amendments made in 2024 by Law No. 7499 aligned the cross-border data transfer regime with the GDPR.

- Cost perspective: “Yet another obligation added.”

- Leverage perspective: Companies that built a KVKK infrastructure close to GDPR compliance were able to send the message “data transfer is secure” to EU customers. Competitors could not.

Regulation turned here into a trust signal that creates a barrier to entry.

E-Commerce Law (6563 → 7416) → Scale Asymmetry

Amendment No. 7416 was designed to limit the market power of large platforms: progressive obligations, licensing requirements, bans on unfair commercial practices. This regulation confirms Stigler’s theory in reverse — regulation was used to restrict the incumbent player rather than protect it.

- Cost perspective: “Licensing cost, compliance burden.”

- Leverage perspective: The restriction of large platforms created market share opportunities for niche players. The progressive implementation schedule (2023-2025) turned this opportunity into a temporal arbitrage window.

Cybersecurity Law (7545) → From Unregulated to Regulated Space

The Cybersecurity Law accepted in March 2025 consolidated the area, which was previously managed by fragmented regulations, into a single framework. Before the law, quality standards were uncertain, and there was severe information asymmetry. After the law, certification requirements turned into a competitive advantage for companies that already offer high-quality services, and a risk of being pushed out of the market for unprepared players.

General rule: The first-time regulation of a field is a structural breaking point where the most prepared actor is rewarded and the least prepared is penalized.

RSM — MOVE: What Should You Do?

- Read regulation through three lenses. Public interest tool (classical), political market product (Stigler), structural leverage (Porter/Bradford). The first two to understand, the third to act.

- Calculate the option value of compliance investment. Compliance cost + non-compliance risk = standard equation. But the option value created by compliance (new market access, customer trust, licensing rights) in most cases justifies the cost on its own.

- Turn early compliance into time arbitrage. If a regulation has a progressive implementation schedule, the window is open. The most prepared actor is rewarded. The unprepared is penalized.

References: Pigou (1920), The Economics of Welfare · Stigler (1971), “The Theory of Economic Regulation,” Bell Journal · Peltzman (1976), “Toward a More General Theory of Regulation,” JLE · Porter & van der Linde (1995), “Environment-Competitiveness Relationship,” JEP · Bradford (2020), The Brussels Effect, OUP · OECD (2012), Regulatory Policy and Governance · Law No. 6698 KVKK · Law No. 7499 · E-Commerce Amendment Law No. 7416 · Cybersecurity Law No. 7545.

⚠️ Legal Disclaimer: This article has been prepared for general information and strategic analysis purposes only. It does not constitute legal opinion and cannot be interpreted as binding legal advice on any matter. For a legal evaluation specific to your situation, it is recommended to consult a specialized legal expert in the field.

LexForesight extracts commercial foresight from regulatory complexity.